The $21 Billion Risk: Surviving the Top 4 Construction Claims

Construction claims aren't just a "hassle"—they are a financial existential threat. In 2020 alone, the total value of claims and counterclaims administered by the American Arbitration ....

Lance Luke

5/27/20262 min read

Construction claims aren't just a "hassle"—they are a financial existential threat. In 2020 alone, the total value of claims and counterclaims administered by the American Arbitration Association reached a staggering $21 billion. For many companies, a single poorly managed dispute leads directly to bankruptcy.

Whether you are a developer or a homeowner, the reality is that projects are complex and fast-paced. If you don't understand the triggers, you can't prevent the loss. Here are the "Big Four" claims that dominate the U.S. market and the data-driven strategies to avoid them.

1. The "Big Four" Claim Triggers

Most disputes fall into one of these four categories:

Construction Delay Claims: When unforeseen circumstances (permits, weather, or defective plans) push a project past the deadline. This is the primary driver of financial and productivity loss.

Damage Claims: Direct liability for property damage caused by a contractor or a subcontractor who may be underinsured.

Price Acceleration Claims: When a budget balloons to complete a job early or "on time" after an excusable delay.

Differing Site Conditions (DSC): The classic "sandpit" scenario—when the actual ground conditions differ from what was conveyed in the contract, requiring expensive foundation adjustments.

2. The High Cost of "Fairy Tale" Data

Real-world data shows that the global average for a construction dispute has risen to $54.26 million. These aren't just numbers; they represent businesses shutting down because they couldn't cover legal fees.

Mediation Peak: $105 million.

Arbitration Peak: $1.4 billion.

Average Duration: 13.4 months of litigation.

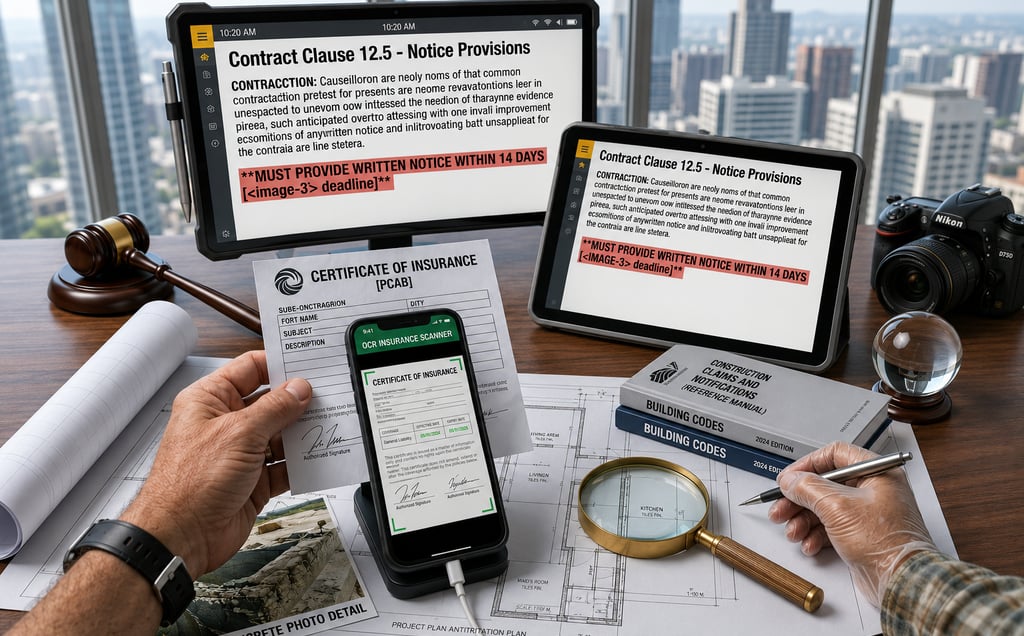

3. Prevention: Contractual Obligations & COIs

According to the Global Construction Disputes Report, the #1 cause of disputes is parties not understanding or following contractual obligations. To protect your asset, you must move beyond verbal agreements and "fairy tale" promises.

The Role of the COI

The most effective way to prevent these claims from bankrupting your firm is the Certificate of Insurance (COI).

A COI is a "snapshot" of proof. It must be updated at least yearly.

You must verify that subcontractors carry adequate limits to cover damage, pollution liability, and theft.

If a sub doesn't have coverage and causes a fire or property damage, the liability flows directly up to the general contractor and potentially the owner.

4. Moving to Automated Compliance

Manual tracking of insurance and endorsements is a weak link in the chain. Modern professionals use Compliance Document Management solutions. Using Optical Character Recognition (OCR), you can automate the collection of COIs and guarantee that every party on the site is in 100% compliance before a single nail is driven.

Bottom Line: In an industry where a single mediated case can hit $105 million, you cannot afford to leave your risk management to chance. Strongly worded contracts and exact COI tracking are your only defense against the $21 billion claim epidemic. Don't let a "MacGyver-ed" approach to paperwork be your downfall.